Testing the Prosperity Loop in a Canonical Economic Model

This page documents an early systems experiment for The Prosperity Loop.

We take a well-known stock-flow consistent macroeconomic model from the textbook Monetary Economics by Wynne Godley and Marc Lavoie, known as Model PC, and extend it with the core structural components of the Prosperity Loop:

A Commons Fee applied to economic output

A National Wealth Fund that accumulates those fees

A Dividend paid from the fund back to households

The key constraint is deliberate. We do not change the original structure of the model. Interest rates, portfolio choice, government spending, and accounting closure remain exactly as in the textbook version.

The question is simple but foundational:

Can the Prosperity Loop be added to a standard post-Keynesian macro model without breaking it?

Why we are doing it

Before asking whether a new economic framework improves equity, resilience, or sustainability, a more basic question must be answered:

Does it actually work inside the accounting logic of the economy?

Stock-flow consistent models are unforgiving. Every dollar must come from somewhere and go somewhere. If a proposal violates those constraints, instability or inconsistency appears quickly.

This experiment is a structural integrity test, not a performance test. Its purpose is to verify that the Prosperity Loop can be implemented as real economic plumbing, not just as an idea or narrative.

What model we are using and why

Model PC is intentionally simple. It includes:

Households

Government

A central bank

Two financial assets, cash and government bills

Portfolio choice by households

A fixed policy interest rate

It does not include firms, profits, investment, or ecological constraints.

That simplicity is a feature, not a bug. It makes Model PC an ideal sandbox for answering one question cleanly:

Does adding the Prosperity Loop preserve macroeconomic stability and stock-flow consistency?

What the graphs show

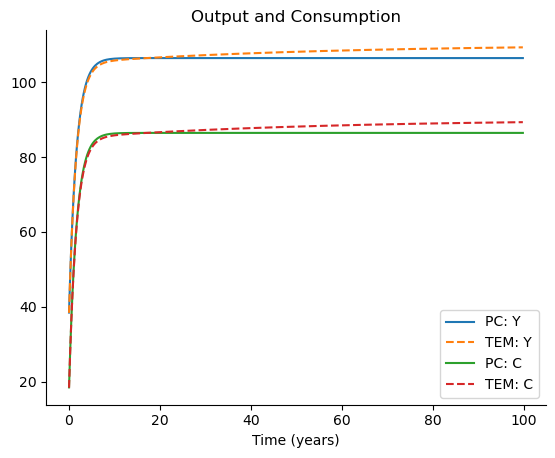

Output and consumption

The extended model and the original model follow nearly identical paths. Both converge smoothly from zero initial conditions to a stable long-run trajectory.

This tells us something important. Adding the Commons Fee, Wealth Fund, and Dividend does not destabilize production or demand when implemented conservatively.

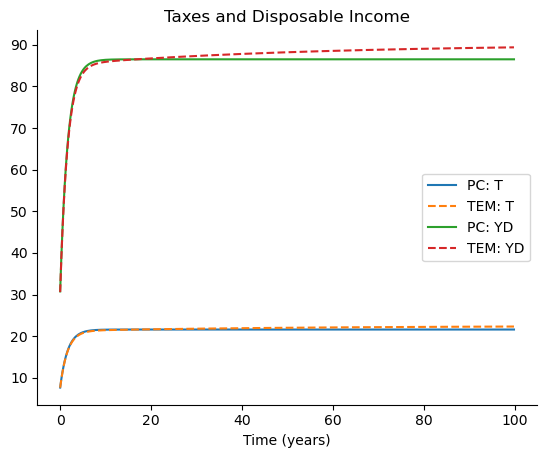

TAXES AND DISPOSABLE INCOME

Disposable income is slightly higher in the Prosperity Loop version once the Wealth Fund matures and dividends begin flowing.

Taxes also rise modestly, because dividends are treated as taxable income. This confirms that the model is internally consistent and fiscally coherent. There are no hidden transfers or accounting shortcuts.

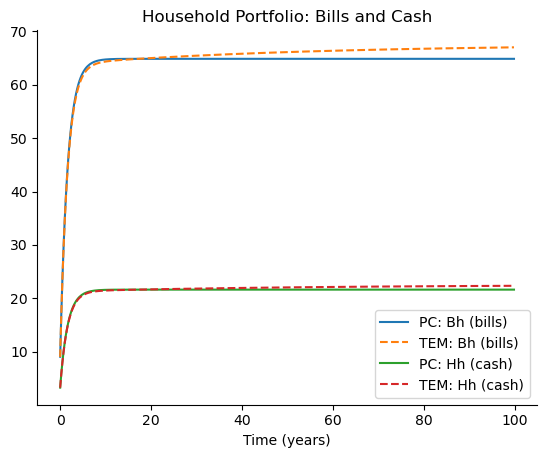

HOUSEHOLD PORTOLIOS

Households hold cash and government bills in nearly the same proportions as in the original model.

This matters. It shows that the Prosperity Loop does not interfere with core monetary mechanics such as portfolio choice or central bank operations. The extension operates above the monetary layer, not inside it.

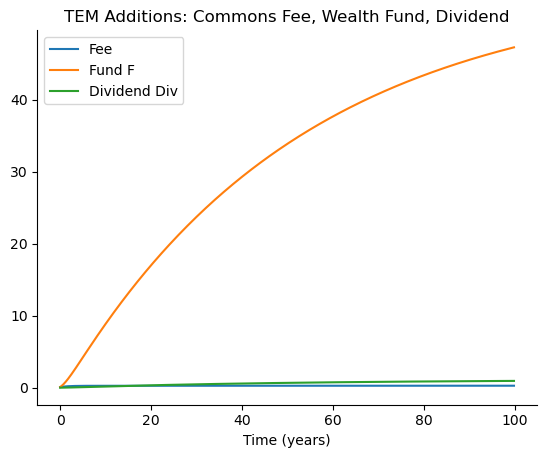

Commons Fee, Wealth Fund, and Dividend

Here we see the new structure clearly:

The Commons Fee scales with economic activity.

The Wealth Fund accumulates smoothly over time.

The Dividend grows gradually as the fund matures.

There are no oscillations, crashes, or runaway dynamics. The fund behaves as a stable long-term stock, and the dividend behaves as a delayed, predictable flow.

This is exactly what a sovereign wealth structure is supposed to do.

What the results mean

The results are intentionally uneventful. That is the success.

They show that:

The Prosperity Loop can be implemented inside a canonical macroeconomic model.

All accounting identities hold period by period.

New stocks and flows are dynamically stable.

Policy levers behave predictably.

No hidden assumptions are required.

In short, the Prosperity Loop passes a basic but essential test of economic realism.

Why this matters for our goals

Claims about equity, resilience, and sustainability only matter if the underlying system is sound.

This experiment establishes a foundation. It shows that the Prosperity Loop can function as part of the real economy’s balance-sheet logic, not as an add-on or exception.

That makes it meaningful to move forward to more complex models that include:

Firms and profits

Investment and retained earnings

Credit dynamics

Ecological constraints

Those models are where equity, resilience, and sustainability can actually be tested.

What this experiment does not show

It is equally important to be clear about limits.

This experiment does not demonstrate:

Redistribution across income groups

Demand stabilization during recessions

Investment responses to commons fees

Ecological limits or regeneration

Long-run sustainability outcomes

Model PC is simply too minimal to express those dynamics. It has no firms, no profits, and no ecological system.

That is why this experiment is a starting point, not a conclusion.

What comes next

The next step is to repeat this process in progressively richer stock-flow consistent models from the same tradition, beginning with Model LP, which includes firms, profits, and investment.

At each step, the same discipline applies:

Add the Prosperity Loop

Preserve accounting closure

Test for stability

Learn what the model can and cannot reveal

This page documents one rung on that ladder.

Explore the model

You can view and run the full Jupyter notebook used for this experiment here:

All code, equations, and assumptions are transparent and reproducible.